All Categories

Featured

Table of Contents

The are whole life insurance policy and global life insurance. The cash worth is not added to the death benefit.

After one decade, the cash worth has actually expanded to around $150,000. He gets a tax-free financing of $50,000 to start a business with his bro. The plan car loan rate of interest price is 6%. He pays off the loan over the next 5 years. Going this route, the passion he pays goes back right into his plan's money value rather than a banks.

Ibc Banking Concept

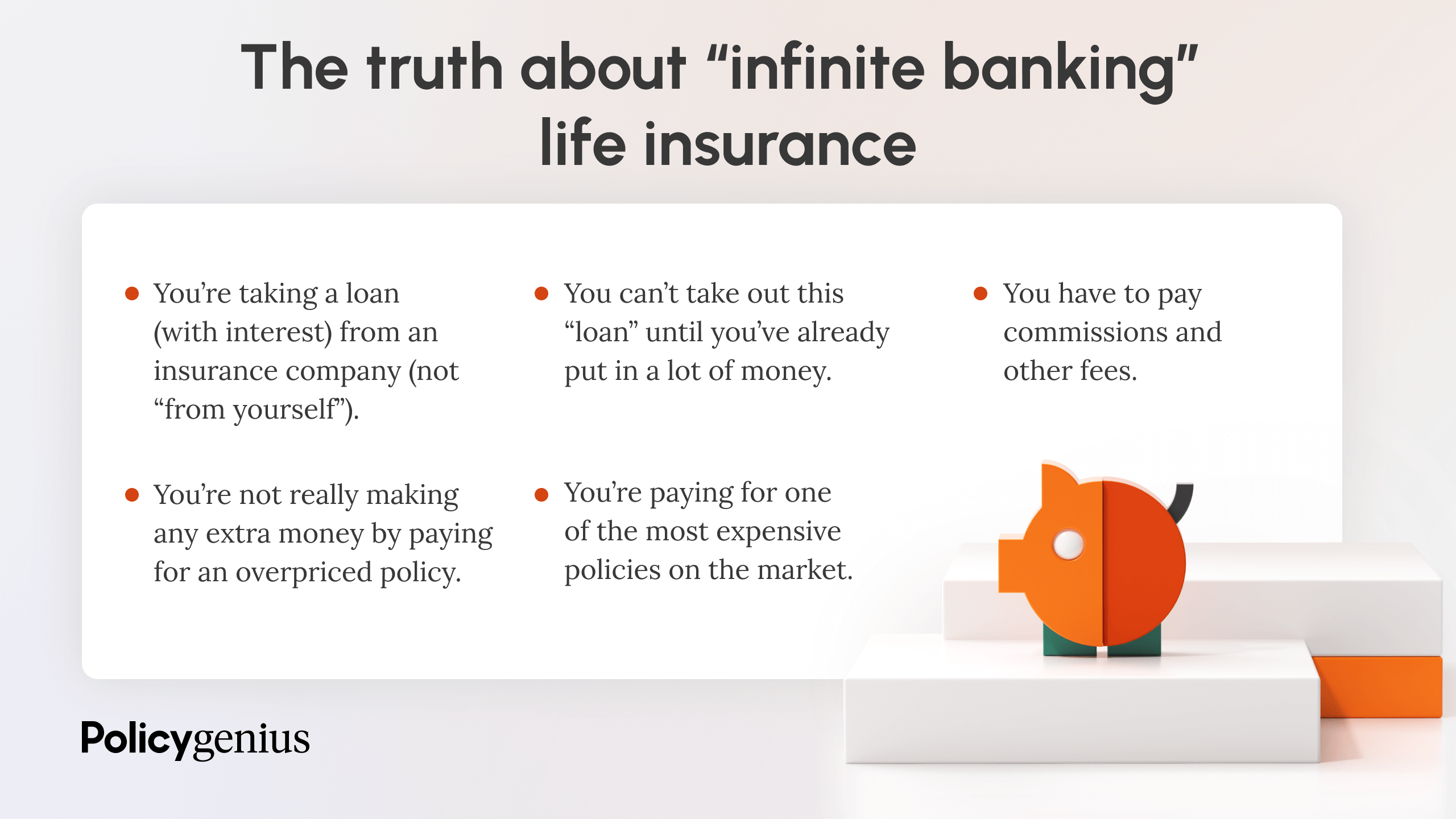

The concept of Infinite Financial was created by Nelson Nash in the 1980s. Nash was a finance specialist and follower of the Austrian school of economics, which advocates that the value of products aren't clearly the outcome of standard economic structures like supply and demand. Instead, people value cash and products differently based upon their financial condition and needs.

One of the risks of standard banking, according to Nash, was high-interest prices on loans. Long as banks set the interest rates and car loan terms, individuals didn't have control over their very own wealth.

Infinite Banking needs you to possess your monetary future. For goal-oriented individuals, it can be the most effective economic tool ever. Here are the advantages of Infinite Financial: Probably the single most helpful facet of Infinite Banking is that it enhances your capital. You don't need to go via the hoops of a conventional bank to get a car loan; simply demand a plan car loan from your life insurance policy business and funds will certainly be provided to you.

Dividend-paying whole life insurance is extremely low danger and provides you, the policyholder, a fantastic deal of control. The control that Infinite Financial supplies can best be grouped into 2 groups: tax benefits and asset protections.

Rbc Infinite Visa Private Banking

When you utilize whole life insurance for Infinite Financial, you get in into a personal agreement between you and your insurance policy firm. These protections might differ from state to state, they can include security from possession searches and seizures, security from reasonings and defense from creditors.

Entire life insurance policy policies are non-correlated properties. This is why they function so well as the monetary foundation of Infinite Financial. Regardless of what occurs in the market (supply, genuine estate, or otherwise), your insurance plan retains its worth.

Market-based investments grow wealth much faster but are revealed to market fluctuations, making them naturally risky. What if there were a third pail that provided safety however also moderate, guaranteed returns? Entire life insurance policy is that 3rd bucket. Not just is the price of return on your whole life insurance coverage policy ensured, your fatality benefit and costs are likewise assured.

Below are its major benefits: Liquidity and availability: Plan financings give immediate accessibility to funds without the limitations of typical bank car loans. Tax obligation effectiveness: The cash money worth grows tax-deferred, and policy finances are tax-free, making it a tax-efficient device for building riches.

Whole Life Infinite Banking

Asset defense: In several states, the money value of life insurance coverage is safeguarded from financial institutions, adding an extra layer of monetary safety and security. While Infinite Banking has its values, it isn't a one-size-fits-all solution, and it includes significant disadvantages. Right here's why it may not be the best method: Infinite Banking typically needs elaborate plan structuring, which can puzzle insurance policy holders.

Visualize never ever having to stress over financial institution fundings or high interest prices again. Suppose you could obtain money on your terms and build riches all at once? That's the power of limitless banking life insurance policy. By leveraging the cash money worth of whole life insurance coverage IUL policies, you can grow your wide range and obtain money without counting on standard banks.

There's no collection lending term, and you have the liberty to choose on the repayment timetable, which can be as leisurely as paying back the funding at the time of death. This adaptability includes the maintenance of the fundings, where you can choose for interest-only payments, maintaining the funding balance level and manageable.

Holding money in an IUL fixed account being credited rate of interest can often be far better than holding the cash on deposit at a bank.: You've always desired for opening your very own bakery. You can obtain from your IUL policy to cover the preliminary expenses of renting a room, purchasing devices, and hiring staff.

Rbc Royal Bank Visa Infinite Avion

Personal finances can be obtained from traditional financial institutions and credit unions. Here are some vital points to think about. Credit report cards can supply an adaptable method to borrow cash for really temporary periods. Borrowing cash on a credit card is generally really costly with annual percent rates of passion (APR) typically reaching 20% to 30% or more a year.

The tax obligation treatment of policy fundings can differ substantially depending upon your country of home and the particular regards to your IUL plan. In some areas, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy lendings are generally tax-free, supplying a considerable benefit. In various other territories, there may be tax obligation implications to take into consideration, such as potential tax obligations on the financing.

Term life insurance just offers a fatality benefit, without any kind of money worth buildup. This means there's no money worth to borrow versus. This short article is authored by Carlton Crabbe, Ceo of Capital forever, an expert in supplying indexed universal life insurance policy accounts. The information given in this article is for academic and informational functions just and must not be construed as monetary or financial investment guidance.

For car loan officers, the comprehensive policies imposed by the CFPB can be seen as cumbersome and restrictive. Loan officers commonly suggest that the CFPB's guidelines produce unnecessary red tape, leading to even more paperwork and slower lending processing. Guidelines like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) needs, while focused on protecting customers, can lead to hold-ups in closing deals and increased functional expenses.

{kind=link}

Latest Posts

Infinite Financial Systems

Infinite Banking Concept Explained

Infinite Banking Illustration